0002 - Entropy and Finding Signal Through the Noise

In February of 2020 I was in our Singapore office, onboarding a new senior director. He had flown in from Australia and planned to spend a few weeks settling in before moving his family out. We were at a real pivot point. After a couple of business model iterations we believed we had found the strongest signal in a combined offer: cybersecurity services with cyber insurance. Now we were laying the foundation to build out the capability and start capturing market share.

About that time there were some reports on the news about a virus in China. But, Singapore was a modern city-state with a reputation for running things well. Daily life was completely normal, and we didn’t think much of it.

In March, a few cases appeared and were quickly contained. Then some buildings started checking your temperature on the way in. Then a few asked you to fill out a quick health questionnaire as well. Then these logistical hurdles were everywhere, seemingly all at once. Getting out of the office, into a cafe to buy food or coffee, and back into the office became a two-hour ordeal. Three months later the entire world was locked down.

By June we had no idea why the new business model wasn't gaining traction. Was the idea flawed? Was selling enterprise cybersecurity over Zoom, with no in-person trust building, simply not going to work? Was the global lockdown causing buyers to freeze budgets? It could plausibly have been any one of those, or all three at once. There was so much noise in the environment that we couldn't decipher the signal.

Building a venture capital-backed start-up is itself a risky, high-entropy undertaking, and because of that, requires a low-entropy environment to test and validate in.

Private Equity, by contrast, invests in stable businesses with steady cash flow. Most of those businesses have already been through multiple economic cycles. They’ve weathered the ups and downs and survived. PE-backed businesses tend to be low-entropy and high-signal, which is what makes them attractive to PE’s debt-heavy approach.

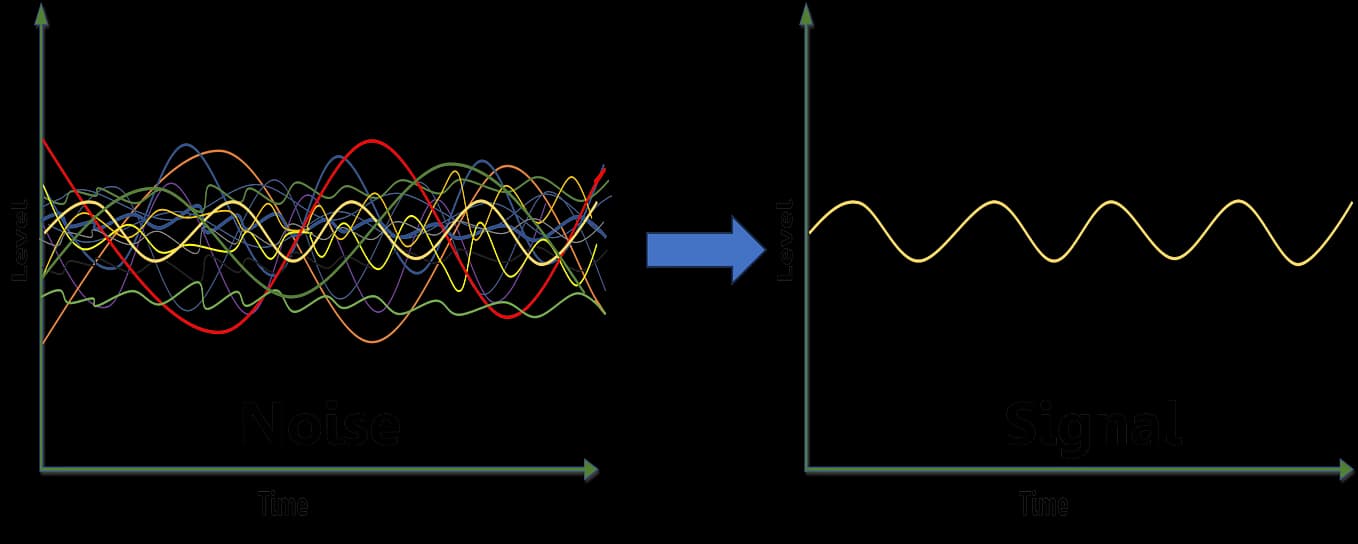

The Signal and Noise Problem

Almost every business activity is fundamentally a signal-through-noise problem. The question is how much noise the environment generates and how much of it the operator has to live with.

Venture capital handles this by tightening variables upstream. The VC playbook is to bet on businesses where as many of the obvious failure modes as possible have been pre-eliminated. A proven market with a known better solution (Uber replacing taxis); a new technology that everyone would want if it became available (GLP-1's); a well-established business model copied into a new geography (Grab mimicking Uber in Southeast Asia); a founder with previous experience, including failure (Reid Hoffman). You can't remove all the noise from an early-stage bet, but you can eliminate the variables that don't have to be in the test.

Private equity goes further. It buys assets that have already cleared the noise floor at the macro economic cycle level: 30 years of operating history, positive cash flow through at least one downturn, and an established customer base. The deal team's job in diligence is to confirm that those macro signals are real. Once they are, the asset itself is, by definition, low-entropy. That's what makes it investable and eligible for adding debt.

Here is the part the operating partner usually finds out afterwards: the asset is low-entropy at the deal level. The operating environment inside the asset usually isn't. The investment thesis ends up testing on data the company can't trust.

That gap is sharpest in the lower middle market, where the smaller PE firms play. But, as money has poured into Private Equity, and more money is chasing fewer companies, even the biggest firms aren’t immune.

Markets As Information Systems

Adam Smith gets credit for describing how markets work in An Inquiry into the Nature and Causes of the Wealth of Nations, but he only describes the first half: incentives. Self-interest, the invisible hand, leads the baker and the butcher to produce your dinner without intending to. But that’s only half of the function of a free market.

Friedrich Hayek named the other half. In The Use of Knowledge in Society, his 1945 essay, he argued that the deeper function of markets is informational. No central authority can ever gather and process the dispersed knowledge of millions of producers and consumers, fast enough, to allocate resources well. Markets do it automatically. Prices are the compressed signal. A price going up tells a stranger on the other side of the country, who knows nothing about you or your situation, that the thing you want has gotten scarcer or more valued. They can act on it without ever knowing why. Price is a perfectly condensed signal.

The Smith frame and the Hayek frame are not in conflict. They are two functions of the same mechanism. Markets provide both incentives and information, simultaneously, through the same price signal. Free market competition is a derivative of incentives and information.

With that theoretical concept in mind, I want to explore it more in the context of a single company.

Every company is itself an information system. It is constantly generating internal signals about its own state. Revenue by segment. Margin by product line. Throughput per technician. Time-to-collect. Customer concentration. Retention by tenure. Win rate by deal source. None of that is hidden, in principle. It is happening, all the time, inside the business. The question is whether the company has built itself in such a way that those signals are legible.

Legibility is the word worth exploring.

For now, I’ll describe signal legibility this way: an operator can ask a question, get the answer in something close to real time, and trust that the answer means what it appears to mean. A signal is illegible when the data exists in principle but takes a week and three people to produce, or when each person who pulls it makes slightly different definitional choices, or when the answer this month and the answer last month were computed by different methods and can't honestly be compared.

Or, when it lives in the heads of key employees and isn’t captured in a system of record.

The investing world and the operating world both depend on legible signals, but they get them in very different ways.

Capital markets have a high degree of legibility. A public company's stock price, its quarterly filings, its bond spread, its credit rating: these are signals the market has spent two centuries building infrastructure to produce, standardize, and transmit. They aren't perfect, but they're legible enough that capital can flow on them, almost frictionlessly, across the world. Hayek’s price-as-information system works because the infrastructure underneath it works.

Inside a lower middle market company, that infrastructure often doesn't exist. The company has signals. It has Janet's gross margin spreadsheet and Dave's intuition about which technicians will be gone in six months vs. those that will stay for years. What it doesn't have is the standardization, the persistence, and the queryability that would let an operating partner treat those signals the way capital markets treat a stock price. You can't act on what you can't trust, and you can't trust what gets re-computed differently every time you ask for it.

Janet and Dave

Take two examples a sub-institutional operating partner will recognize immediately.

Janet works in accounting. She has been at the company for eleven years. If you ask her for gross margin per account she can produce it. She has run that pull a hundred times and her spreadsheet is accurate. If you ask her for the same gross margin sliced by customer segment, she gets visibly annoyed, because she has to rebuild the data manually from a couple of source files that don't share a clean customer-segment field. If you ask her for that segmented view every month, on the same definition, so you can see trends, she stops being annoyed and starts being upset. Each month means each month, by hand, with her doing the definitional reconciliation manually, every time.

The data is there. Janet is there. The infrastructure to ask new questions of the data, repeatedly and consistently, isn't.

Dave runs the technician team. He has been doing it for fifteen years. He can tell you, within a job or two, how many service calls a week each of his guys can handle. He can call which technicians are going to leave in the next 90 days with a confidence that would make an HR analyst nervous. His operating intuition is probably worth six figures a year to the company.

If you ask Dave for the data behind any of it, the answer is roughly the same: it's in PDFs, in folders, organized by month and year, on a shared drive. If you ask him for technician churn by tenure bucket over the last 24 months, he can give you the qualitative shape from memory, but nobody can produce the actual number. If Dave leaves, the intuition leaves with him. The pattern recognition exists at the human layer. The data layer can't see it.

Janet and Dave have something important in common: the people have the operating intuition; the system has none of it.

Every lower middle market company has a Janet and a Dave, and often a few of each. The company is big enough to have real complexity, multiple customer segments, dozens of employees, real revenue, but small enough that the founder ran it on instinct for twenty years before the PE check cleared. The instinct is the system. The investment thesis assumes you can test the company independently of the instinct. You can't… yet.

The Analyst-and-AI Raid

The most common operating partner response when they realize they can't get the data they want is some version of the analyst-and-AI raid. Bring in two analysts, start collecting and dumping files into Claude, run a four week discovery sprint, surface a few patterns nobody knew were in the data, put them into a slide deck, and declare visibility achieved.

It's worth being fair to this move. Discovery work, done by a skilled analyst with AI tools can produce real findings. The company genuinely did not know that segment B has half the gross margin of segment A. The pattern is real, the analysis was honest, the slide deck is not theater.

What the raid doesn't do is lower the noise going forward.

A discovery is a snapshot, typically built on messy and incomplete data. It tells the operating partner what the company looks like at a moment in time. Next quarter, when a new question arrives (we lost three accounts in segment C, why?), Janet is still annoyed and Dave's PDFs are still in folders. The analyst is gone. The deck the discovery produced is already stale, and nobody has the standing assignment to refresh it. The next question gets answered by the next raid, on a new budget, two quarters later.

This is why most "AI initiatives" in lower middle market portcos quietly die within a year. The discovery was real. The instrumentation to act on the next twenty questions, continuously, was never built. Discovery alone produces a report, not a capability.

The structurally different move is much less photogenic. It looks like building the systems that both capture historical patterns and continue to track them, so the next question, and the one after that, and the one after that, can be asked and answered without another raid. The operating partner who insists on this is not the one who looks fastest in month three. They are the one who can actually test the investment thesis in month eighteen.

To be fair: AI has gotten really good. It can handle messy data, and it seems to be getting better every month. Do you actually need to spend time cleaning up source systems, building a data warehouse, and layering on semantic definitions? My answer to that is this: AI tokens convert energy into statistical computations. Companies that spend the time to structure their data well will get exponentially better returns on their AI spend compared to companies that don’t. That advantage will compound as data increases and AI gets better.

The Thesis Is Being Tested on Noise

Six months into the Singapore experience we had to live with not knowing whether the model was broken, the medium was broken, or the world was broken. That was a once-in-a-century environmental noise event, and it eventually cleared. Most operators never have to navigate anything that severe.

The muted version of the same question, though, is permanent for an operating partner. It shows up every month, on every portco in the fund, and the honest answer is usually: we still can't tell.

If you want to find out whether you're in that position, ask yourself a few diagnostic questions:

- When this month's numbers surprise the CEO, how long until you know whether the surprise is worth acting on?

- If you wanted gross margin by customer segment for the trailing 24 months, on a consistent definition, could you get it this afternoon? Could you get it next quarter, on the same definition, without anyone re-doing it by hand?

- When a key person left last quarter, did the data see it coming, or did you find out at the exit interview?

If the answers are “not sure”, "not really," or "eventually," then the asset you bought may have higher entropy than the operating environment you're testing it in, and you may struggle to find real signal through the noise.