Issue 0003: You Are the 81%

AI value capture is an operating-model problem. The modern gold rush is real, but unless you're Nvidia, Anthropic, or OpenAI, you are not selling shovels.

You are at the quarterly business review: the CFO has just walked through working capital and the COO has just walked through inventory turns. Now you come to the obligatory AI slide. It has three bullet points: how we are using it, where we are using it, what we are going to do next. You already have Claude Pro subscriptions for the leadership team and there’s some debate about whether to extend it to the back office. Should we pay to train the staff on it? Should we do it in-person or online? What’s our budget for this? Someone makes a claim that it is "doubling efficiency" in some unspecified function. Nobody asks what doubled, or what was halved, or how it was measured.

The deck itself was probably generated with Claude. You can tell by the em dashes punctuating every paragraph as if a comma or colon simply wouldn’t do. There is a sweeping closing slide about transformation and the future of work.

Someone asks about ROI and the answers come back in sequence. Top-line impact? Not yet. Cost cutting and improved net margins? Not yet, but soon. Anything we can tie to a specific dollar? Well, no, but the technology shift is generational. We have to be doing this or we will be disrupted.

The meeting moves on.

AI In the Enterprise: Two Surveys

If that describes your last QBR, you are not alone. You are in good statistical company.

McKinsey's State of Organizations 2026 surveyed 10,000 senior executives across 15 countries and 16 industries. They found that 88% of organizations are now deploying AI in some way. Of those, 81% report no meaningful bottom-line impact. The deployment number is going up but the impact number is not. The gap between companies deploying AI and those seeing real returns is widening, not closing.

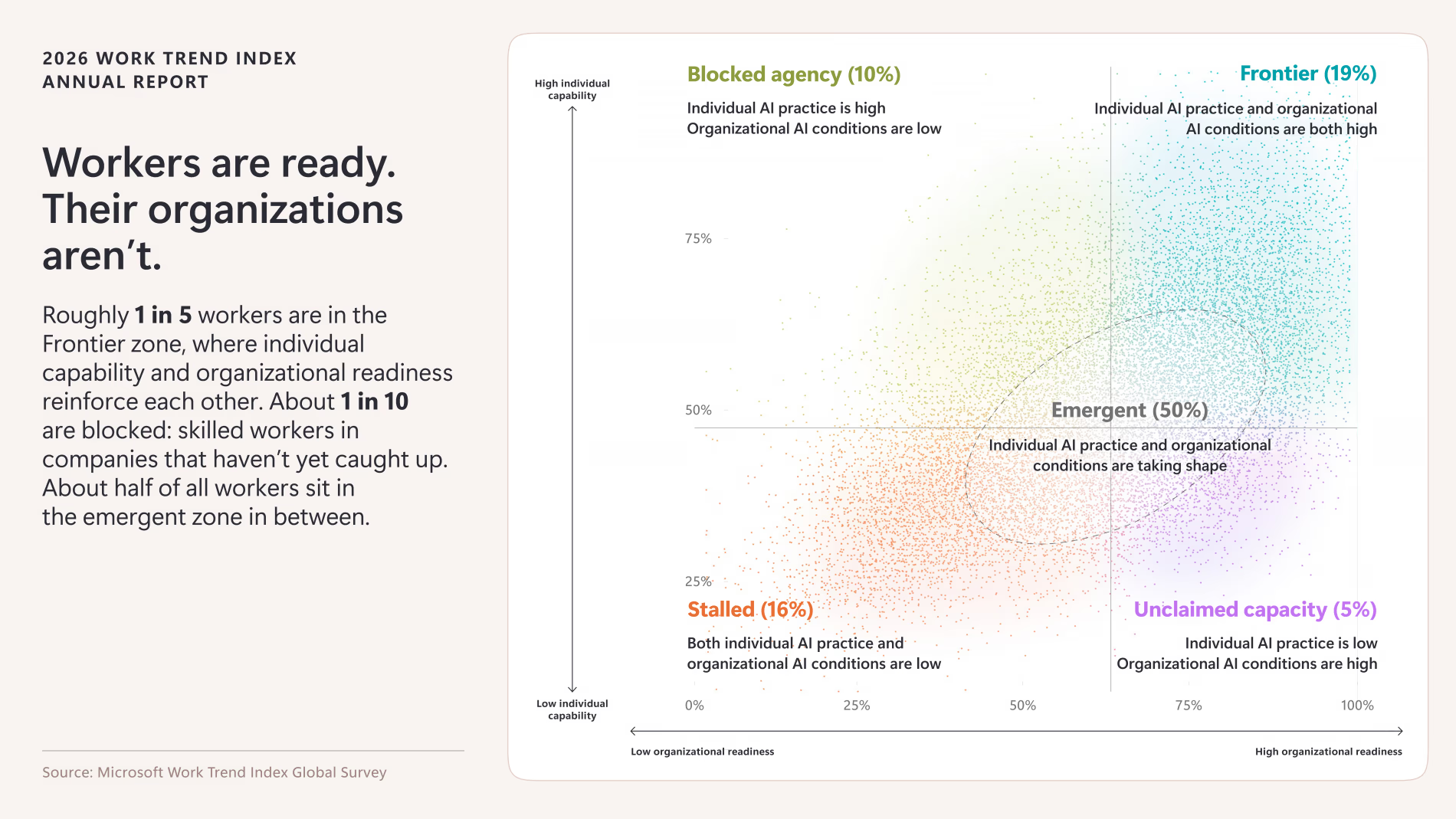

Microsoft's 2026 Work Trend Index, published in May, arrives at the same diagnosis from a different angle. They surveyed 20,000 knowledge workers who already use AI at work and mapped each one across two axes: individual AI capability and organizational readiness to absorb it. Only 19% of respondents landed in the zone Microsoft calls "Frontier," where individual capability and organizational systems reinforce each other. 50% sit in an emergent middle. 16% are stalled on both axes. 10% have built the individual skills but have no organizational system to put them to work.

The 81% and the 19% are not measuring the same thing, exactly. McKinsey is measuring reported bottom-line impact. Microsoft is measuring how organizational readiness affects worker productivity. They are different lenses on the same question, and they converge on the same answer. Roughly one in five organizations is actually capturing the value of the AI it is buying. Roughly four in five are not.

(Microsoft just killed its Claude Code program because of run-away spending, indicating they’re in the 81%, too. So maybe you want to take their “insights” with a grain of salt)

The Microsoft data goes further: after testing 29 organizational, individual, and demographic factors against self-reported AI impact, the analysis concluded that organizational factors account for 67% of AI impact, and individual factors account for 32%. The single strongest variable was the organization's AI culture. The top three factors were all organizational and had nothing to do with the skill of the individual AI users. Just hiring a few “AI native” workers won’t get you where you need to be.

We have two independent surveys, with two methodologies, and one conclusion: the constraint on AI value capture is not the model’s capabilities, it’s the capabilities of the organization buying the model.

Three Readings of the Data

This data admits three possible readings:

- 81% of businesses do not know how to use AI well. The technology works; the buyers are slow.

- AI is not actually that useful to most businesses. The buyers are reasonable; the technology is overhyped.

- AI is useful to businesses that know how to absorb it, and most businesses do not. They lack the infrastructure to deploy it, the visibility to measure it, and the operating discipline to know whether it is working. For these businesses, AI becomes another SaaS subscription, indistinguishable from the last fifteen. Or worse, something that can drive runaway costs.

I believe the third reading is the one the data actually supports.

The hyperscaler capex is real. Frontier model capability is impressive. The capture failure is not a technology problem, it is an integration and absorption problem. That means the answer is not "buy more AI" and not "wait for the technology to improve." The answer is more basic and is upstream of both.

Wait and See

The strongest case against acting now is that wait-and-see is actually rational.

The technology is still maturing. Inference costs are falling roughly an order of magnitude per year. The capability gap between frontier models and open-source models is closing. Tooling that was bespoke in 2024 is becoming a commodity in 2026. If you wait two years, the same capability will cost a fraction, the integration will be easier, and the failure modes will be better understood. Why not let the early adopters absorb the experimentation cost of being early?

This is a defensible position. However, I believe it is also wrong in a specific way.

The foundational work that converts AI capability into business impact does not depend on AI capability. It depends on whether your business has clear KPIs, a well-structured data layer for the numbers on those KPIs, and a reporting cadence that makes the numbers visible to the people who can act on them. None of that requires AI. It can take 6 to 18 months to build, depending on how much technical debt you currently have.

If you wait until 2028 to take AI seriously, you will spend 2028 building the foundations you could have built in 2026. The model providers will have shipped four more capability generations, and you will not be able to really benefit from any of it, because the underlying business does not have the visibility to point those capabilities at anything specific.

Wait-and-see does not save you time. It defers the foundational work and guarantees you stay in the 81% when you finally make the move.

The Modern Gold Rush

It helps to put this cycle in historical context.

In January 1848, James Marshall found gold at Sutter's Mill in California. Over the next seven years, roughly 300,000 people moved west to dig for it. Most of them did not get rich. In 1849, the early arrivals were averaging about twenty dollars a day, which was many times the prevailing wage but not millionaire money. By 1853, the average daily yield had fallen to under six dollars. After 1853, mining was mostly unprofitable for independent operators, and most miners either left or signed on as wage laborers for the industrial mines that the bankers had built.

The fortunes were made elsewhere. California's first millionaire was Samuel Brannan, who never mined a day in his life. He ran general stores in San Francisco and Sacramento and sold supplies to the miners. At his peak, his stores were turning over $150,000 a month in 1850s dollars ($6.3M/month in 2026). Levi Strauss arrived in 1853 to sell dry goods, and eventually, jeans. The bankers, the shippers, the assayers, and the landowners earned far more reliable money than the miners did.

The lesson from this for most businesses is not "sell shovels." The lesson is that the people who got rich selling shovels did not need to know where the gold was. The miners did, and most miners did not.

The same shape is repeating now. The chip makers, the hyperscalers, and the frontier model providers are selling shovels. Nvidia, OpenAI, Anthropic, Google, xAI, and the cloud providers underneath them. They do not need to know where the gold is in your business. You do. And as the McKinsey and Microsoft data show, most companies do not.

If you are operating a PE-backed portfolio company in the lower middle market, you are almost certainly not in the shovel-selling position. The shovel category is locked up by a small number of trillion-dollar entrants. You are a miner, and you have three options.

- Buy the shovels and start digging like everyone else. You’ll join the 81% seeing no real top or bottom line impact.

- Ignore the rush entirely, in which case you give up the foundational work that compounds whether or not the technology lives up to its hype.

- Do what the 19% are doing. Build the infrastructure that lets you see where the gold actually is in your specific business, so the shovels you buy can be used to dig in the right places.

The Levels Are the Operator-side Answer

That third option is what the Aptum AI Levels Framework is built around. The framework names five operating states and the transitions between them:

- L0: Visibility

- L1: Reporting Spine

- L2: Decision Guidance

- L3: Operating Cadence

- L4: Compound Leverage

The first two transitions are the foundational work that does not depend on AI capability. Once those are in place, the places where AI can deliver real value become more clear. Until they are, every AI initiative ends up being just another SaaS subscription.

I have written about the Levels framework in more depth here. For the purposes of this piece, the relevant point is that the 19% are not the 19% because they bought better AI. The same AI technology is fully available to everyone. They are in the 19% because they did the foundational work that lets them point AI at the right problems. The 81% are the 81% because they did not.

Three Questions for Your Next QBR

When the AI slide comes up at your next QBR, three questions are worth asking before the deck moves on.

-

What specific KPI did this AI initiative move last quarter, and by how much? If the answer is "we don't have a clean baseline," that is the foundational gap, restated. You cannot capture value you cannot measure. Said differently: if you were to limit or cap your AI spend, where would you direct its use, and where would you remove it?

-

What decision is being made differently because of AI that was not being made differently before? If the answer is "we are using it for productivity," you are in the 81% using AI for productivity within existing structures. That is not value capture. That is overhead with extra steps.

-

Whose annual compensation moves if the AI program works, and whose moves if it doesn't? If no one's comp moves, no one owns it. If no one owns it, you are not running an AI program, you are running an AI line item.

The three questions land where the data lands. The capture problem is upstream of every vendor decision, and it is solvable by people who are willing to look at it honestly. The companies that do the foundational work can get real value from the technology, with increasing returns as it matures.

The companies that buy the technology before doing the foundational work get to keep spending money on it and keep padding the fortunes of the shovel-makers.

You are probably in the 81%. That is not a verdict, it’s a starting point.